Quarterly Agricultural Update | January 2026 - March 2026

Thu 02 Apr 2026

Brown&Co’s market update provides an overview of commodity prices for 2026. It also provides an overview of points to consider going forward into Spring 2026, which include Environmental Schemes, Grants and UK Agricultural Policy updates.

Summary

The Brown&Co Agricultural Update Report reviews the previous financial quarters, highlighting the changes in market prices and trade patterns of commodities during the period.

This report analyses the cereals, oilseeds, milk, and meat prices, as well as input prices such as fuel, fertiliser, and feed.

- The Standard Pig Price (SPP) has decreased in quarter one, finishing at 182.70 pence per kilo deadweight (p/kg/dw) compared to 198p/kg/dw at the end of the previous quarter.

- Defra farmgate milk prices have continued to decrease this quarter and averaged 36.07 pence per litre (ppl) in February 2026, a decrease of 3.49ppl since the close of the previous quarter (December 2025).

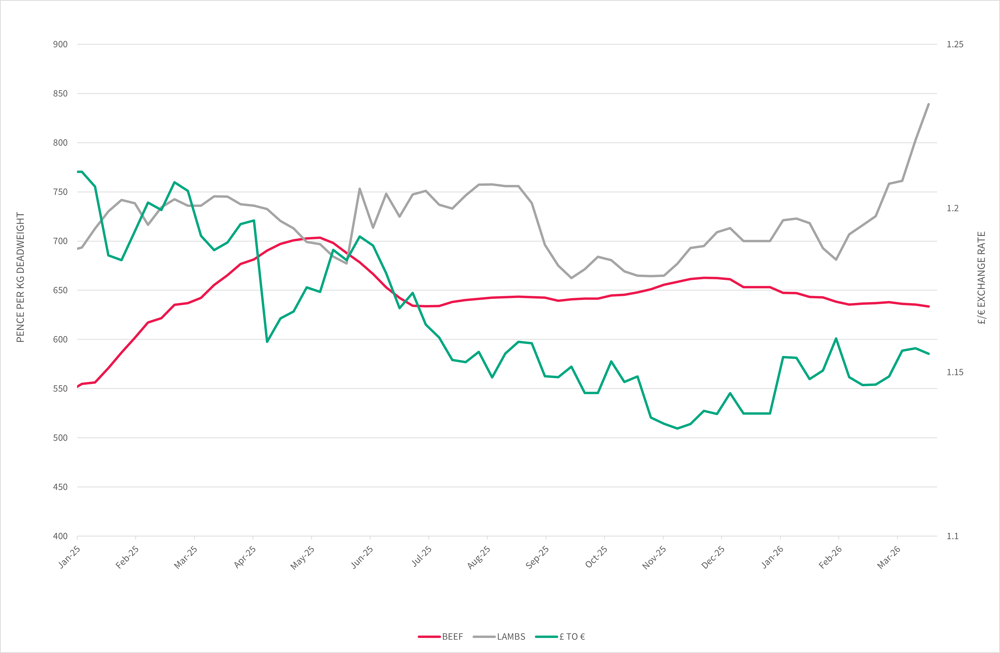

- Lamb prices experienced an increase in price over quarter one, ending on 839.20p/kg/dw (R3L), an overall increase of 139.20p/kg/dw from the end of the last quarter.

- The falling beef prices for All Steers has continued throughout this quarter. Prices finished the quarter at 633.60p/kg/dw for all steers, a 19.6p/kg/dw decrease compared to the end of last quarter.

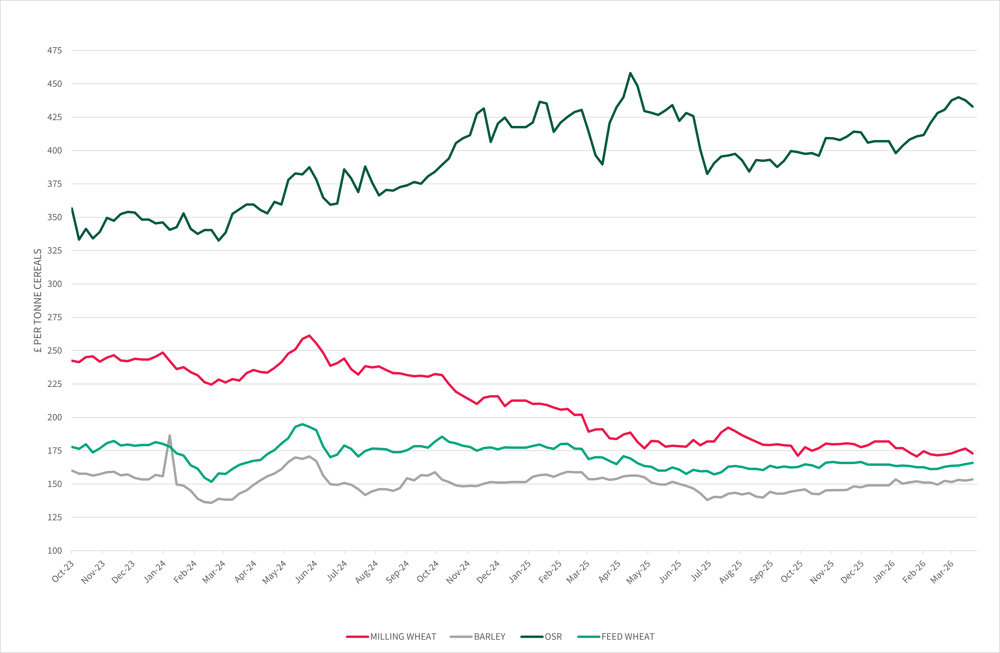

- Cereal & Oilseed markets have been mixed, the feed wheat price has been relatively static, ending the quarter at £165.90/tonne, compared to £164.60/tonne at the end of the previous quarter. Milling wheat price has seen an overall decrease in price, ending the quarter at £173/tonne, with a milling premium of £7.10/tonne. Oilseed rape has experienced a steady increase over the quarter, closing at £433/tonne, an increase of £26.10/tonne from the end of the last quarter.

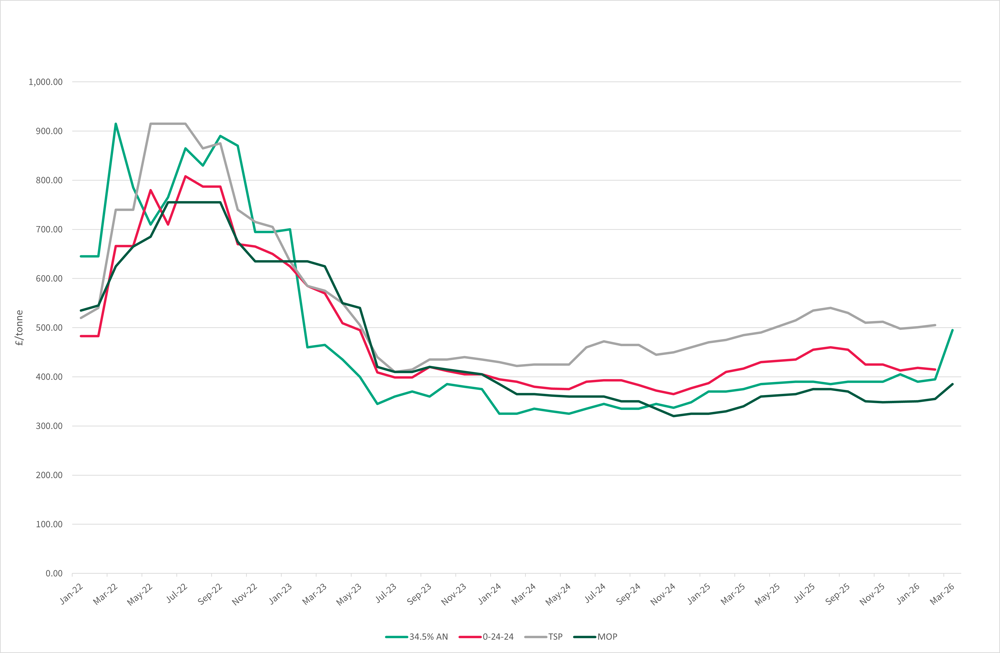

- Overall, fertiliser prices have increased over the quarter. 34.5%AN started the quarter at £405/tonne and ended the quarter at £495/tonne, a £90/tonne increase. MOP has seen a £36/tonne increase since the end of the last quarter. The spot price for 0-24-24 and TSP was unable to be given for March 2026 meaning orders are limited due to the turbulence and unsettledness in the Middle East and fertiliser needing to pass through the Strait of Hormuz.

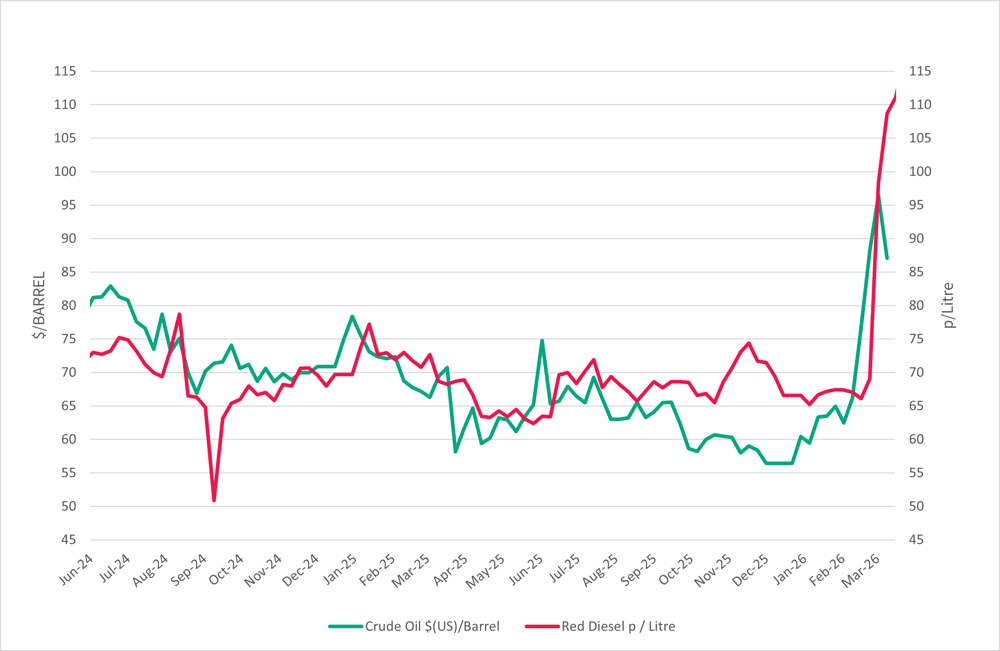

- Red Diesel saw an increase of 50.52 pence/litre across the quarter ending at 117.08 pence/litre. An increase of 75.9%. Crude Oil saw an increase of 30.62 $/barrel across the quarter ending at 87.07 $/barrel. An increase of 54.25%. The fuel prices dramatically increased this quarter, driven by the instability in the Middle East, particularly the conflict involving Iran.

Points to consider

Environmental Schemes

At the NFU’s Annual Conference on 24th February 2026, Emma Reynolds, Secretary of State for Environmental, Food and Rural Affairs made a series of announcements with a focus on clarity, partnership, transparency and growth.

In March, the first meeting of the Farming and Food Partnership Board took place, key objectives to oversee sector growth plans, starting with horticulture and poultry. This board will be a fundamental reset between the government, farming and food sectors. The board is one of the recommendations from Baroness Batters farming profitability review.

British agriculture is being promoted through trade deals with the US, meaning British beef now has exclusive access to the American market for the first time. A 13 thousand-tonne quota, allowing opportunities to 300 million more customers.

Details of the SFI offer:

- Reduction in the number of actions from 102 to 71.

- Agreement cap of £100,000 per year.

- Only one SFI26 agreement per business.

- Removal of the management payments for new agreements - integrated pest management plan, nutrient management plan and soil management plan, plus the agreement management payment.

- The combined area of ten actions limited to 25% of the farmed land for SFI26 now also includes AHW7: Enhanced over winter stubble. This limit is applied across all SFI agreements to the holding.

- Increasing payments for moorland actions in both new and existing agreements to ensure hill farmers are properly compensated.

- Reducing rates of 3 key options - see table below.

| Action | Previous Rate | New Rate | Change |

|---|---|---|---|

| CSAM3: Herbal leys | £382/ha | £224/ha | −£158/ha (−41%) |

| CAHL2: Winter bird food | £853/ha | £648/ha | −£205/ha (−24%) |

| CNUM3: Legume fallow | £593/ha | £532/ha | −£61/ha (−10%) |

Full scheme details will be published before the scheme opens, with clear budgets set for each window and no sudden and unexpected closures.

Two SFI application windows:

- June – Small farms 3 - 50 hectares and those without existing ELM revenue agreements.

- September – the scheme will open up to all other eligible businesses.

Careful planning for new SFI26 agreements will be essential, particularly for businesses currently managing multiple SFI23, Expanded Offer and Countryside Stewardship agreements. Consolidating these schemes into a single SFI26 agreement is likely to create funding gaps for some businesses. Although the £100,000 per year agreement cap is reported to affect only 3% of existing SFI agreement holders, this estimate does not take into account those who also hold Countryside Stewardship agreements, which will in time transition into SFI26. As a result, it is anticipated that a higher proportion of businesses will be impacted by the cap once all existing environmental schemes are combined into a single SFI26 agreement.

Grants

Capital Grants to reopen in July, with up to £225 million available, £50 million more than last year.

Productivity Grants have been allocated £120 million for 2026:

- £50 million for the Farming Equipment and Technology Fund (FETF)

- £70 million for the Farming Innovation Programme to aid productivity through research

Farming Equipment and Technology Fund (FETF)

FETF 2026 opened for applications on 17th March and will close 28th April, with £50 million available to help farmers invest in equipment that improves productivity, animal health and welfare, and slurry management.

The 3 themes are:

- Productivity equipment (£20 million available)

- Animal health and welfare (£20 million available)

- Slurry management (£10 million available)

Grants are available between £1,000 and £25,000 per themes, with a maximum of £75,000 available if a business applies for all 3 themes.

£1 billion will be invested into a new national biosecurity centre at Weybridge, this research will aid to protect farmers and food producers by having the capability to handle any future animal disease threat.

There have been over 11,000 funded vet-led reviews for cattle, sheep and pig farmers; showing the evidence that early intervention works with disease prevention and spread. From this summer, these visits will be extended to poultry.

The RPA confirmed that almost 80% of farmers offered an extension to their Countryside Stewardship Mid-Tier agreements have accepted, equating to 4,000 agreements worth just under £60 million.

UK Agricultural Update

The Office for Budget Responsibility (OBR) forecast predicts input costs to be 30% higher in 2026 than they were in 2022. When the UK left the EU in 2020, the Farming Budget was not increased with inflation meaning the £2.4 billion figure for farming in England has nearly been the same since 2007.

On 27 January, the major pig and poultry feed manufacture ABN announced it was looking to sell off a number of sites. ABN, part of AB Agri, a subsidiary of Associated British Food (ABF), lost a major feed contract with 2Agrilcuture in April 2025. The concerned mills are Flixborough near Scunthorpe, Cullompton in Devon, and Langwathby in Cumbria, potentially totalling 115 redundancies if a buyer is not found. ABN have made this decision following a comprehensive review; taking action to secure the long-term sustainability of the business.

The Iranian conflict has sharply increased UK farmers’ costs—especially fuel and fertiliser—due to disruptions around the Strait of Hormuz, and this has tightened already fragile farm margins while creating major uncertainty for future planting and production decisions. Looking ahead, UK agriculture will need to plan for continued volatility in global energy and fertiliser markets, reassess input use, and strengthen resilience through policy clarity and supply‑chain transparency. Rising red diesel prices—up about 75%—and fertiliser costs driven by higher gas prices and disrupted global trade have already forced farmers to rethink cropping strategies, input levels, and financial planning. If tensions persist, farmers may face further price spikes, reduced availability of key inputs, and pressure on yields, while future challenges include navigating Environmental Land Management Scheme reforms, improving energy efficiency, and building more robust domestic supply chains to reduce exposure to geopolitical shocks.

COMMODITY PRICE COMPARISON BETWEEN MARCH 2025 & 2026

| Produce | Measurement | March 2025 |

March 2026 |

Difference | % Change |

|---|---|---|---|---|---|

| Lamb | P/KG/DW (R3L) | 741.0 | 790.4 | 49.4 | 6.3% |

| Beef | P/KG/DW (ALL STEERS) | 659.9 | 635.8 | -24.1 | -3.8% |

| Pork | P/KG/DW (SPP) | 203.9 | 184.5 | -19.4 | -10.5% |

| Milk | P/L | 45.85 | 36.07 | -9.8 | -27.1% |

| Wheat (Feed) | £/TONNE | 169.0 | 164.6 | -4.4 | -2.7% |

| Barley (Feed) | £/TONNE | 153.8 | 152.6 | -1.2 | -0.8% |

| Oilseed Rape | £/TONNE | 405.2 | 437.0 | 31.8 | 7.3% |

| £ TO € Exchange | GBP to EUR | 1.1909 | 1.1546 | -0.036 | -3.1% |

Note: Due to the dynamic period we are currently in, commodity prices may move daily.

UK Weather

January

January began with a brief but notable cold spell across the UK, with Scotland experiencing widespread frosts and snowstorms during the first week. Conditions then turned wetter and more unsettled, marked by a succession of impactful storms. Storm Goretti on the 8th and 9th brought damaging winds to Cornwall and significant snowfall across Wales and the West Midlands. Later in the month, Storm Ingrid generated large waves along the Devon and Cornwall coastline on the 24th, washing away a historic pier. This was followed by Storm Chandra on the 26th and 27th, which delivered heavy rain and strong winds to the Southwest, causing flooding in Devon and Somerset due to already saturated ground. Overall, the UK’s mean temperature for January was 0.5°C below average, while rainfall was notably high, reaching 117% of the long‑term average. Cornwall recorded its wettest January on record, with 195.6 mm of rain.

February

February was characterised by exceptionally mild yet notably dull conditions across the UK, delivering some of the lowest sunshine totals on record. Despite the lack of brightness, it ranked as the ninth warmest February on record, with 21 counties reporting their highest February minimum temperatures, reflecting unusually mild nights. Rainfall was also significantly above normal at 70% above the long‑term average, contributing to the West Midlands, Leicestershire and Cornwall recording their wettest winter on record. Persistently saturated ground left many areas increasingly vulnerable to flooding. Climate experts note that warmer air can hold more moisture, leading to heavier downpours, and recent trends show increasing rainfall totals on the UK’s wettest days, with a clear shift toward wetter winters—particularly across western regions.

March

March saw slightly above-average temperatures, with England trending around 10–12°C through the month and conditions gradually warming as spring approached. March brought a mix of dry spells and frequent rainfall, with England typically seeing around 14–19 rainy days and 49–62 mm of precipitation, alongside only a light scattering of snow in some areas. Sunshine levels remained modest at around 4 hours per day, and winds were generally breezy, averaging 18 km/h. The drier conditions were seen in the south and southeast, while more changeable weather with rain and stronger winds affected northern and western regions later in the month. Overall, March delivered a typical early‑spring pattern: mild, unsettled, and gradually brightening as the month progressed.

Harvest 2026

Autumn 2025 largely followed the summer dry weather theme, meaning many were able to drill winter crops with some of the best winter drilling conditions for quite some time.

One proven difficulty was with Winter Oilseed Rape, with the lack of rain making it difficult to plan effectively the best window to drill for successful germination. While a wet winter has persisted, most winter crops have been sown into good seedbeds allowing successful establishment to withstand the waterlogged conditions.

Climate & Carbon

2026 represents a pivotal year for the UK’s climate and sustainable finance agenda, driven by three major areas of progress: strengthening the framework needed to grow the green economy, improving regulatory disclosure standards to enhance the quality and consistency of corporate reporting, and integrating climate and industrial policy to support a more strategic approach to national decarbonisation.

In January, the National Wealth Fund (NWF) published its Strategic Plan, outlining how it will deploy capital to accelerate long‑term growth and expand clean energy investment, including targeted measures to derisk sectors such as energy storage and battery manufacturing.

Alongside this, the Net Zero Council and the Transition Finance Council are working to identify investment gaps, clarify transition pathways and improve visibility around delivery risks, with the aim of boosting investor confidence and enabling more efficient capital allocation.

The year is also critical for shaping the UK’s Seventh Carbon Budget, due in June, which will be informed by Climate Change Committee advice and will set the emissions strategy for the 2030s. This budget is expected to guide investors towards projects and technologies aligned with the UK’s long‑term net zero objectives.

Supply Chain

On 20th February, the US Supreme Court ruled that key elements of the Trump administration’s tariff regime introduced on 4th April are unlawful, throwing the US trade policy into disarray. For UK agriculture, this has renewed the uncertainty around US trade policy and what that means for planning, pricing and credibility of current deals, including the UK-US Economic Prosperity Deal (EPD), agreed in May 2025. The implications include direct exposure to tariffs, with exports to the US accounting to 11% of export revenue for 2025 of agri-food goods. Under the EPD, the UK is subject to a 10% tariff for most goods and whilst the UK is confident that EPD will continue to stand despite the US Supreme Court ruling, this still remains unconfirmed, meaning that UK goods could face 15% tariffs making them less competitive.

Additionally, there are indirect effects via global markets, rapidly changing US tariffs and trade policy can disrupt the global markets. Exporters facing more barriers into the US will turn to alternative importers with more consistent policies. This could potentially intensify competition in major import markets, including the EU and UK, for the UK this could result in a downwards influence on some farm-level prices. The trade policy uncertainty looks to continue under the US administration, highlighting the need for traders to undertake sensitivity analysis on tariff levels on the trade with the US.

Consumer Behaviour

Quarter one saw consumers remain financially cautious, responding to ongoing economic pressures with a heightened awareness of how they spend, discover and engage with brands. Confidence in the wider economy stayed low, prompting people to be more deliberate in their purchasing decisions. While spending did resume, it did so cautiously, with consumers closely scrutinising price, convenience and perceived quality, and withholding purchases when expectations were not met. Data indicates that this level of scrutiny has now become embedded in consumer behaviour and is expected to persist throughout the remainder of 2026.

Livestock Markets

Dairy

Global dairy markets entered 2026 with abundant supply, supported by strong milk production across major exporting regions and lower feed costs that encouraged continued output despite weakening prices.

Since late 2025, dairy prices have fallen sharply, particularly for fat‑based products: butter declined by more than 40% between September and February, while whole milk powder fell by around 30%, reflecting oversupply and more cautious purchasing. Protein markets have been comparatively stable, with prices down roughly 15% overall, though trends within the category have diverged—skimmed milk powder has strengthened since January, and whey prices continue to rise on the back of strong demand for high‑value protein ingredients.

Recent Global Dairy Trade auctions indicate early signs of recovery, but current supply levels remain too high to support a sustained rebound. Milk production growth among the Big Seven exporters is expected to slow significantly, from 2.6% in 2025 to just 0.2% in 2026, with a slight contraction forecast for early 2027, signalling the first steps toward rebalancing the global dairy market.

Pork

UK pig meat consumption is expected to continue rising in 2026, supported by steady retail demand and the relative affordability of pig meat compared with other protein options.

However, UK production is forecast to reach 972,000 tonnes, a slight decline of 0.3% from 2025. Breeding pig numbers are also anticipated to fall, driven in part by expected legislative changes to pig housing that may influence producer decisions. Trade conditions are likely to remain volatile throughout 2026, with geopolitical tensions and ongoing disease outbreaks contributing to continued turbulence in global pig meat flows.

Beef and Lamb Price

Lamb

While UK lamb consumption volumes are forecasted to be steady for 2026 due to household budgets remaining tight, exports are forecasted to grow, supported by robust EU market conditions along with imports increasing due to improved market access.

The average lamb price (R3L) for March 2026 is 790.40p/kg, a 49.4p/kg increase compared to March 2025.

Beef

A combination of constrained supply and consumer demand have driven cattle prices to historic highs. After the record high in May 2025, farm prices have edged lower while shelf prices keep rising.

Prices have finished the quarter at 633.60p/kg/dw for all steers, a 19.6p/kg/dw decrease compared to the end of last quarter.

£/€ EXCHANGE RATE IN COMPARISON TO BEEF AND LAMB PRICE

Feed

Feed Prices (£/tonne)

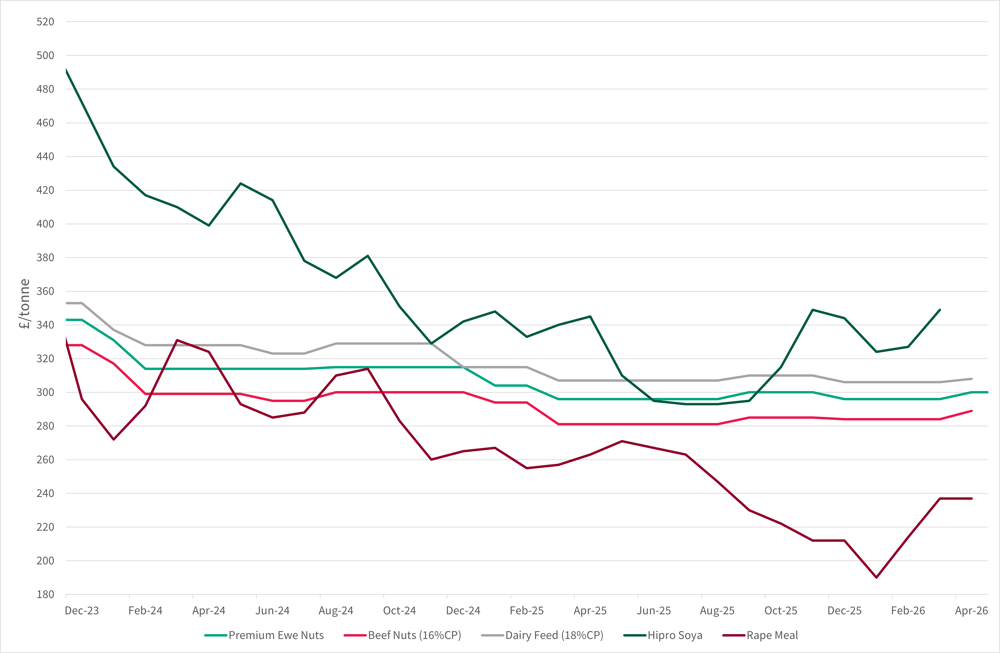

Premium ewe nuts, beef nuts and dairy feeds all remained stable in price with no change across the quarter.

Rape meal price has increased by £18/tonne, compared to the previous quarter which showed a £40/tonne decrease. The changes in price are largely due to global supply, increased demand, and potential changes in trade policies. Specifically, larger soybean harvests in South America and a potential US-China trade deal have contributed the price changes.

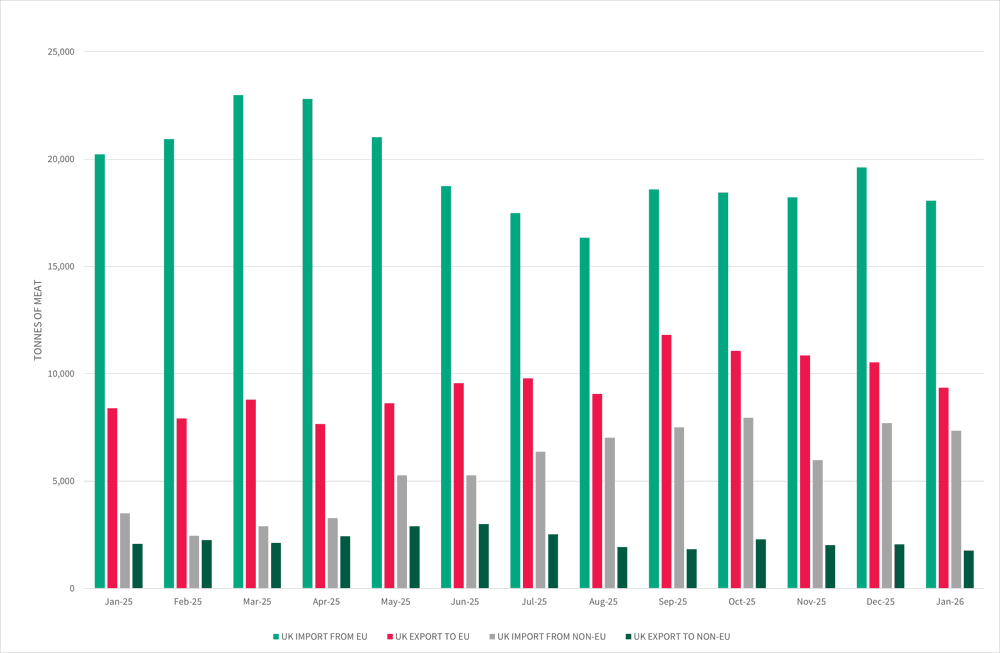

Beef Meat Trade

The UK imports from EU decreased by 2,166 tonnes between January 2025 and January 2026 – a decrease of 10.7%. Unsurprisingly, UK imports from non-EU have seen a steady increase to make up for the loss of tonnage. In January 2025, 3,499 tonnes were imported, compared to 7,349 tonnes in January 2026, a 110% increase in non-EU imports. The UK remains a net importer.

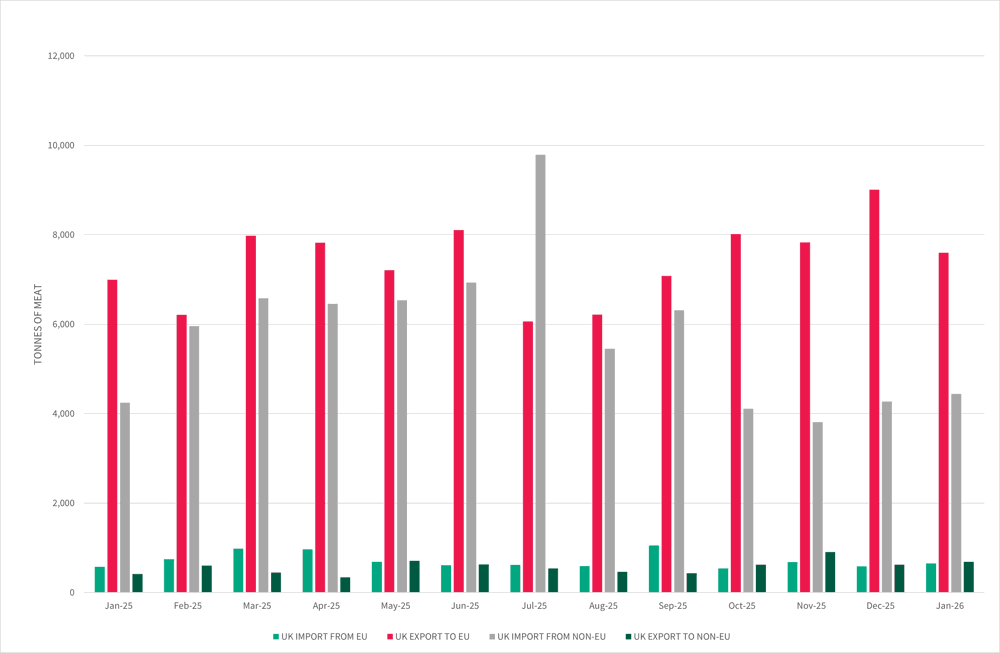

Sheep Meat Trade

The most significant shift for sheep meat, is the 40% increase in UK export to non-EU countries from January 2025, with 414 tonnes and January 2026 with 689 tonnes. Similarly, UK imports from the EU increased from 575 tonnes in January 2025 to 651 tonnes in January 2026, an increase of 12%. The UK was a net exporter for sheep meat in January 2026, with a net balance of 3,192 tonnes.

Wheat, Barley and OSR Price Trends

Feed wheat price has been relatively static, ending the quarter at £165.90/tonne, compared to £164.60/tonne at the end of the previous quarter.

Milling wheat price has seen an overall decrease in price, ending the quarter at £173/tonne. The milling premium continues to tighten, ending the quarter at £7.10/tonne.

Oilseed rape has experienced a steady increase over the quarter, closing at £433/tonne, an increase of £26.10/tonne from the end of the last quarter.

Futures Market

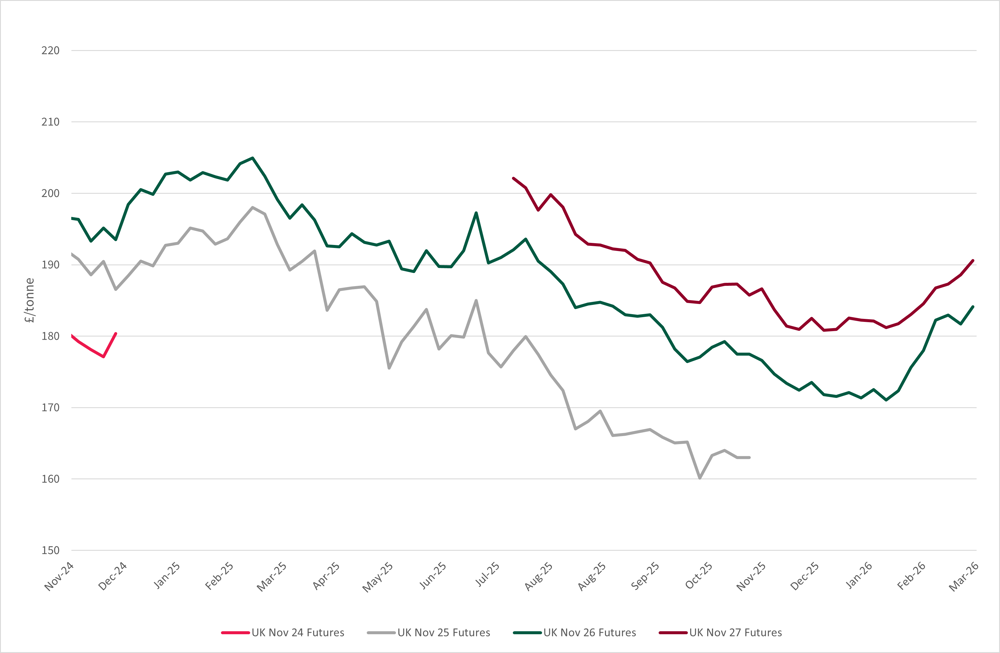

UK Nov Feed Wheat Futures

Both November 2025 and November 2026 wheat futures increased at a similar rate, closing the quarter for November 2026 at £184.10/tonne, an increase of £10.60/tonne and November 2027 at £190.6/tonne, an increase of £8.10/tonne.

Inputs

Fuel & Oil Prices

Both Crude Oil and Red Diesel prices have dramatically increased this quarter driven by the instability in the Middle East, particularly the conflict involving Iran.

Red Diesel saw an increase of 50.52pence/litre across the quarter ending at 117.08pence/litre. An increase of 75.9%.

Crude Oil saw an increase of 30.62 $/barrel across the quarter ending at 87.07 $/barrel. An increase of 54.25%.

Fertiliser

Fertiliser Price Trends

Overall, fertiliser prices have increased over the quarter.

34.5%AN started the quarter at £405/tonne and ended the quarter at £495/tonne, £90/tonne increase, 22%. MOP has seen a £36/tonne increase since the end of the last quarter.

The spot price for 0-24-24 and TSP was unable to be given for March 2026 meaning orders are limited due to the turbulence and unsettle in the Middle East and the fertiliser needing to pass through the Strait of Hormuz.

Brown&Co have one of the largest Agricultural Business Consultancy teams in the country. We are a very practical, down to earth firm who take real pride in our clients’ success and our team’s professionalism.

For proactive and professional services contact your local experts.

Keep updated

Keep up-to-date with our latest news and updates. Sign up below and we'll add you to our mailing list.