Agricultural Update April - June 2026

Wed 08 Jul 2026

Brown&Co’s market update provides an overview of commodity prices for 2026. It also provides an overview of points to consider going forward into summer 2026, which include Environmental Schemes, Grants and UK Agricultural Policy updates.

The Brown&Co Agricultural Update Report reviews the previous financial quarters, highlighting the changes in market prices and trade patterns of commodities during the period.

This report analyses the cereals, oilseeds, milk, and meat prices, as well as input prices such as fuel, fertiliser, and feed.

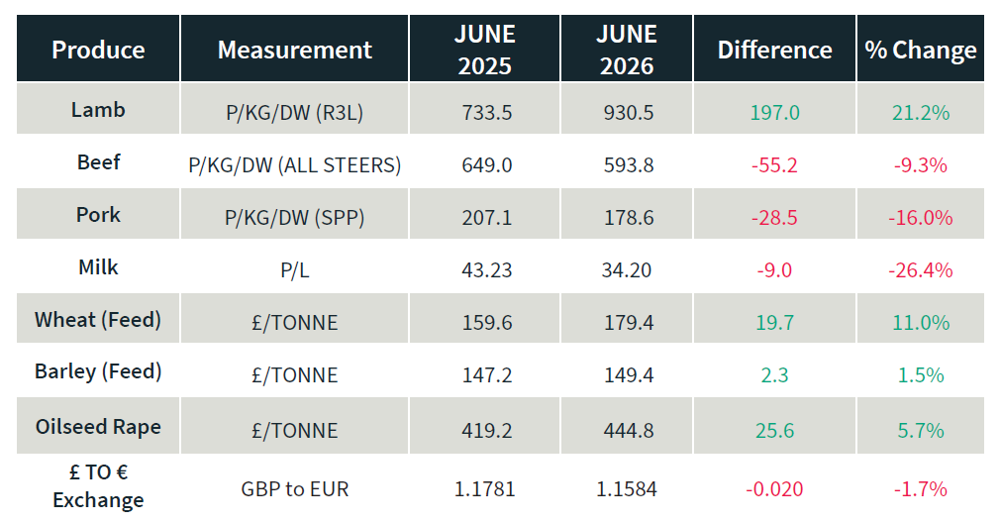

The Standard Pig Price (SPP) has decreased in quarter two, finishing at 178.1 pence per kilo deadweight (p/kg/dw) compared to 182.7p/kg/dw at the end of the previous quarter.

Defra farmgate milk prices have continued to decrease this quarter and averaged 34.20 pence per litre (ppl) in May 2026, a decrease of 1.41ppl since the close of the previous quarter.

Lamb prices experienced an increase in price over quarter two, ending on 907p/kg/dw (R3L), an overall increase of 67.8p/kg/dw from the end of last quarter.

The falling beef prices for All Steers has continued throughout this quarter. Prices finished the quarter at 595.6p/kg/dw for all steers, a 38p/kg/dw decrease compared to the end of last quarter.

Cereals markets have been mixed, the feed wheat price has been gradually increasing, ending the quarter at £177.70/tonne, compared to £165.90/tonne at the end of the previous quarter.

Milling wheat price has followed the feed wheat trend, increasing, ending the quarter at £186.8/tonne. The milling premium has fluctuated over the quarter, ending at £9.10/tonne. Oilseed rape price increased at the first half of the quarter, but then continually decreased during the second half, closing at £427.1/tonne, a decrease of £5.90/tonne from the end of the last quarter.

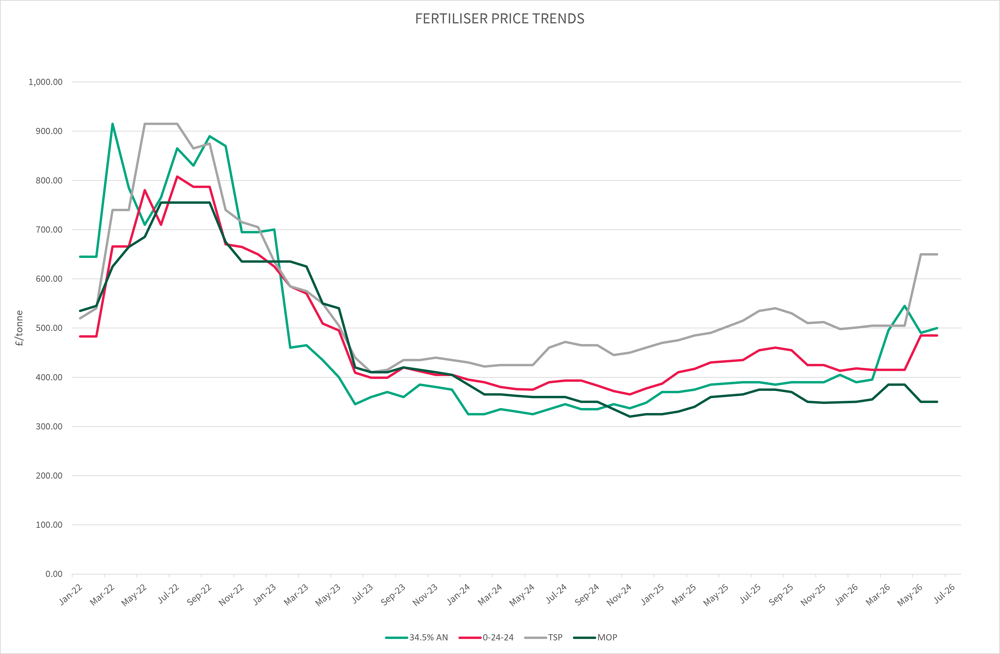

Fertiliser prices on the whole have fluctuated over quarter. 34.5%AN started the quarter at £495/tonne and ended the quarter at £500/tonne, £5/tonne increase but has highs of £545/tonne in May. TSP has had the most dramatic increase starting the quarter at £505/tonne and ending at £650/tonne, up 28% due to the turbulence and unrest in the Middle East and the fertiliser needing to pass through the Strait of Hormuz.

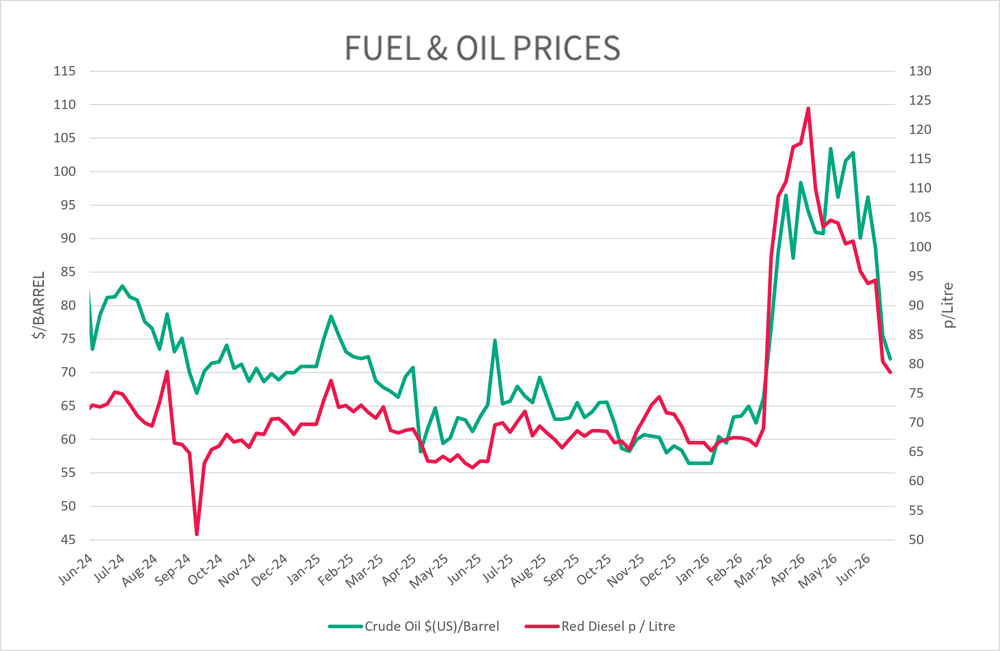

Red Diesel ended the previous quarter at 117.08pence/litre, the price peaked early into quarter two in mid-April at 123.66pence/litre, however, the price continued to come down ending the quarter at 78.58pence/litre, a decrease of 38.5pence/litre. Crude Oil saw a peak price of $103.43/barrel at the start of May 2026, however, has ended the quarter at $72.01/barrel, $15.06/barrel less than at the start of the quarter despite the highest prices mid quarter.

POINTS TO CONSIDER

Environmental Schemes

SFI26 Window 1 opened on 30 June 2026. A few key points which have changed since SFI24 Expanded Offer:

- Agreement cap of £100,000 per year.

- Only one SFI26 agreement per business.

- Removal of the management payments for new agreements - integrated pest management plan, nutrient management plan and soil management plan, plus the agreement management payment.

- The combined area of ten actions limited to 25% of the farmed land for SFI26 now also includes AHW7: Enhanced over winter stubble.

- Land used to grow maize is no longer eligible for the CIPM4 (No use of insecticide) action under the SFI26 scheme. Payment rate £45/ha.

- AWH9 (Unharvested cereal headlands) has now been restricted to headlands only, with a maximum width of 24 meters. Payment rate £1,072/ha.

- SOH1 (No-till farming) has been streamlined, meaning that it allows sowing of all seeds rather than being restricted to cash crops only. Payment rate £73/ha.

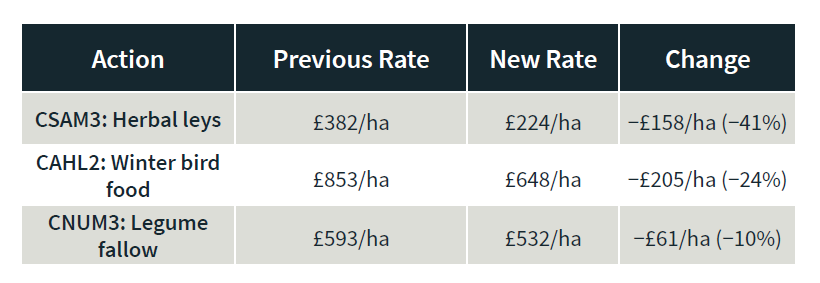

Three key options have had their rates reduced for SFI26:

Two SFI application windows:

- June – Small farms 3 - 50 hectares and those without existing ELM revenue agreements.

- September – the scheme will open up to all other eligible businesses.

Careful planning for new SFI26 agreements will be essential, particularly for businesses currently managing multiple SFI23, Expanded Offer and Countryside Stewardship agreements. Consolidating these schemes into a single SFI26 agreement is likely to create funding gaps for some businesses.

The RPA announced that they are working on a functionality in the application process to enable applying for options/land in existing ELM revenue agreements that are due to expire. This includes SFI23, Countryside Stewardship Mid Tier (CSMT), Legacy CS Higher Tier (CSHT), and Environmental Stewardship Higher Level Stewardship (HLS). Usually, these farmers would not be able to access the full SFI26 offer until their existing agreement expires. This is because many SFI26 actions would:

- be incompatible with what’s in their existing ELM revenue agreement

- mean paying twice for the same output on the same land, at the same time (known as ‘double funding’)

In response to feedback from farmers and stakeholders, they intend to help farmers with soon-to-expire ELM revenue agreements to access the full SFI26 offer. Functionality is being developed on the SFI26 application service to allow farmers to apply for land covered by these agreements before their existing agreements expire. It is expected to be in place from the start of Window 2 in September 2026.

Grants

At the start of June, Defra announced a Poultry Biosecurity Review, part of the Animal Health and Welfare Pathway – a funded vet visit designed to give practical, tailored, site-specific advice to mitigate from bird flu. To be eligible, the business must be responsible for the day-to-day care of the bird, have both a Single Business Identifier (SBI) and have a registered County Parish Holding (CPH) in England. The minimum flock size is between 500-1000 birds depending on the poultry.

Businesses will be able to choose their own vet to undertake the following:

- Look at the biosecurity risks on the site

- Identify where changes could reduce disease risk

- Give tailored advice the business can act on

- Provide a written report for future reference

All funded visits must be completed by 31 December 2028, and claims must be submitted by 31 March 2029. The grant amount is £430 per review to help cover the cost of the visit.

FETF

Farming Equipment and Technology Fund (FETF) 2026 application window was extended to 12th May to support farming businesses invest in equipment and technology that can improve:

- Productivity

- Animal health and welfare

- Slurry management

The RPA also reassured applicants that the scoring thresholds would only be used if applications exceed the available funding and the overall level of demand in that round.

Capital Grants

Capital Grants are to reopen in late July, with up to £225 million available, £75 million more than last year. It is anticipated that these grants will again be popular with farmers and land managers, and pre-application planning is important. Some Catchment Sensitive Farming Officers (CSFO) are already at capacity for applications for prior approvals for this summer’s application window, meaning any options without CSFO support at the point of application will not be eligible in this round of funding.

Agriculture Update

Fuel Duty Rate Reduction

On 20 May 2026, the Chancellor announced a temporary cut in the duty on red diesel. Effective from 15 June 2026 to the end of the year, the fuel duty rate on red diesel will be cut by over a third from 10.18p to a reduced rate of 6.48p per litre. The Government has also confirmed an extension to the 5p fuel duty cut for the remainder of 2026. This is welcome news as fuel prices are inflating production costs across the agricultural sector.

U.S Winter Wheat: Record-Low Acreage hammered by frost damage

Currently the U.S winter wheat crop is enduring its most difficult season in decades. The total wheat area planted for 2026 stands at just 43.8 million acres, this is the lowest since records began in 1919. This is due to overproduction coupled with lower commodity prices and rising input costs, meaning that farmers are turning to more profitable corn and soyabean production.

What began with cautious optimism has unravelled fast. A warm winter pushed crops weeks ahead of schedule, leaving them dangerously exposed when spring cold snaps struck. Frosts in March, April, and again in May tore through Kansas, Nebraska, Oklahoma, and Colorado during critical growth stages. Combined with a severe drought covering 71% of winter wheat growing areas, the yield potential of wheat crops has been reduced.

Markets have reacted with a gradual rise on futures following this most recent market update.

Renters’ Right Act 2025

The Renters’ Right Act (RRA) 2025 came into force on 1 May 2026 which is a substantial change to residential tenancies in England for both existing and new tenancies. For existing AST (Assured Shorthold Tenancies), Landlords must have provided Tenants with an ‘Information Sheet’ by 31 May 2026, with no need to have a new agreement drawn up. For new APTs (Assured Periodic Tenancies) starting on or after 1 May 2026, Landlords must provide a ‘Statement of Terms’ written, setting out the terms of the tenancy.

The main changes under the new APT tenancies compared to previous ASTs are:

Security of tenure strengthened: Section 21 ‘no fault’ evictions will be abolished. Landlords must rely on mandatory grounds such as rent arrears, anti social behaviour, selling the property, or moving themselves or close family in (not within the first 12 months).

Employment linked tenancies: Landlords who provided accommodation as part of employment can regain possession under specific employment related grounds.

No more fixed term tenancies: All tenancies will become periodic (typically rolling monthly). Tenants must give 2 months’ notice to leave.

Rent increases limited: Rent can only be raised once per year, with 2 months’ notice on a prescribed form. Increases must reflect open market value and can be challenged by tenants.

Advance rent capped: Landlords may charge a maximum of one month’s rent in advance.

Pet requests protected: Tenants can request to keep a pet, and landlords cannot unreasonably refuse.

Rental bidding banned: Landlords and agents cannot invite or encourage higher rental bids.

Anti discrimination rules: New protections will prevent discrimination against tenants with children or those receiving benefits.

Effect on Agricultural Workers and Tenancies

Lettings for agricultural workers can be more complex than most other rural tenancies. If the agreement is not set up correctly, the worker can gain an Assured Agricultural Occupancy (AAO), allowing long term security of tenure. To avoid this, employers have traditionally been advised not to use Service Occupancies for farmworkers. Instead, they typically use an Assured Shorthold Tenancy (AST) and serve an Agricultural Notice (Form 9) beforehand, preventing an AAO from arising. This approach previously allowed landlords to end the tenancy using a Section 21 notice.

With the Renters’ Rights Act 2025 abolishing Section 21, from 1 May 2026, ending a tenancy will now be more difficult. However, landlords should still be able to regain possession under Ground 5C, which applies when the tenant was employed by the landlord and the property was provided as part of that employment. If the worker’s employment ends, the landlord can use this ground, provided they give two months’ notice before applying to the court for possession.

To rely on Ground 5C, the tenancy must be set up correctly. A prescribed notice (Form 24) must be served on the tenant before the tenancy begins, confirming that the tenancy is an Agricultural Property Tenancy (APT). Existing Form 9 notices already served for current ASTs will remain valid, helping prevent those tenancies from becoming AAOs.

Political

Portsmouth South MP Stephen Morgan has been appointed as the new Defra Farming Minister, replacing Dame Angela Eagle following a ministerial reshuffle triggered by changes in the defence and security briefings.

His official title is Minister of State for Food Security and Rural Affairs at Defra.

Farming Roadmap 2050

On 24 June, Defra published their Farming Roadmap 2050: Growing England’s Future, setting out a long-term framework for English farming to be more profitable, productive, sustainable and resilient by 2050, whilst providing farmers with greater clarity to adapt, plan and invest. The roadmap collates government commitments for food production; creating fairer supply chains, innovation, climate resilience and farm business performance. It builds on the transition from previous EU subsidies to a market-focused system whilst balancing the three core pillars of food production, farm profitability and environmental recovery.

Note: Due to the dynamic period, we are currently in, commodity prices may move daily.

UK Weather

April

April began unsettled with regular showers and below average temperatures. The frequent showers continued throughout the month, with Storm Dave bringing heavy rains particularly to Scotland and Northern Ireland, with strong winds spreading along the UK. For the second half of the month, high pressure dominated resulting in the mean temperature being 1.1°C above average of 9°C and the seventh warmest April on record. Rainfall varied, Scotland was wetter than average at 117%, whilst England only saw 38% of the expected. Sunshine was widely above average, making it one of the sunniest on record, along with several eastern counties experiencing one of the driest Aprils on record.

May

May 2026 stands out as a warm and seasonally settled month for much of the UK, particularly in the south and east. The clear north–south divide in both temperature and rainfall reflects a stable atmospheric pattern that favoured sunny, warm conditions in southern England and cooler, more unsettled weather in northern regions. Overall, the month continued the trend of above average spring temperatures observed in recent years. The month culminated in record-breaking temperatures on the 25th and 26th May, when the UK daily maximum temperature record of 32.8°C was eclipsed on successive days by at least 2°C, with the final provisional new record being 35.1°C recorded at Kew Gardens, London on 26th May. In total 172 new highest daily maximum temperature records for stations were set between the 22nd and 28th May with 30°C exceeded on seven out of eight days between the 23rd and 30th May. Amber heat health alerts were issued for parts of central, southern and eastern England during this period, although no extreme heat warnings were employed.

June

June was marked by exceptionally high temperatures, ranking among the warmest Junes on record for mean, maximum and minimum temperatures. During the first half of the month, the UK was largely influenced by a westerly Atlantic pattern, bringing in low-pressure with cloudy and unsettled weather. Around mid-month, conditions began to change as high pressure built over continental Europe, drawing much warmer air northwards towards the UK. The second half of June will likely be remembered for an exceptionally hot and humid heatwave, which brought record-breaking June temperatures and unprecedented overnight warmth to many areas. The record-breaking daytime temperature of 37.7°c was recorded in Lingwood, Norfolk on 26th June and a provisional new Wales maximum temperature of 35.9°C recorded at Cardiff, Bute Park on the 25th June.

Harvest 2026

Spring crops in the UK had a relatively good start to the season and largely looked well. That said, growers on lighter land were in need of rainfall. The lack of rainfall in late spring added pressure to struggling crops, reflected in the AHDB’s crop condition report at the end of March. 82% of winter wheat was rated to be looking good or excellent, decreasing to 75% by the end of April. On the other hand, winter oil seed rape on the whole coped better with the drought conditions; 78% was rated good or excellent in late May, compared to 52% at the same time in 2025. The lack of rain saw combines firing up ahead of schedule with early barley combining starting on 26 June on Norfolk-Suffolk border.

Climate & Carbon

Recent government changes to Biodiversity Net Gain (BNG):

BNG requires most developments in England to deliver a minimum 10% biodiversity uplift, measured using Defra’s statutory metric. This uplift can be delivered on site or off site, with off site provision offering a potential long term (30 year) income stream for landowners. Recent policy changes alter both the scope of BNG and the mechanisms through which it is delivered.

- Exemption for Small Sites (<0.2ha)

- Developments under 0.2 hectares are now exempt from BNG

- Defra estimate this will reduce demand for off-site units by 10%

- Reflects the downward pressure on demand

- Greater Flexibility for Minor Developments (<1 ha)

- Minor developments will be permitted to use off-site units without first maximising on-site delivery

- Intended to reduce long-term management burdens for smaller developers

- Likely to increase demand for off-site units

- Shift from Local Planning Authority (LPA) Boundaries to Local Nature Recovery Strategies (LNRS)

- Off-site BNG will be guided by LNRS priorities rather than towards LPA agendas

- LPA must consider LNRS when approving BNG plans

- The biodiversity metric is being revised and may give greater weighting to LNRS-aligned habitat creation

- BNG Extended to Nationally Significant Infrastructure Projects (NSIPs) from November 2026

- Applies to major transport, energy and water infrastructure

- The sale of future demand is uncertain, as any NSIPs may deliver BNG on-site

While the exemption for small sites will reduce demand, this is likely to be outweighed by increased flexibility for minor developments, the strategic shift to LNRS based delivery, and the future inclusion of NSIPs. Overall, the changes point towards a more coordinated, potentially expanding market for off site BNG over the medium to long term.

Supply Chain

Trade and geopolitics

Businesses continued to focus on diversifying trade routes and supply sources due to changing tariffs and wider geopolitical uncertainty. New regulations, including China’s supply chain security rules, have increased compliance requirements and government oversight.

Operating costs remain high

Fuel, energy and industrial materials continued to be the main pressure points for supply chains, keeping costs elevated despite some easing in freight and trucking markets.

Automation accelerating

Ongoing labour shortages and manual workload pressures have pushed businesses to invest more quickly in robotic picking and dock automation.

Consumer Behaviour

Consumer confidence increased slightly with Centre for Economics and Business Research data despite a mixed public mood in June, the same month Prime Minister Kier Starmer announced his resignation. Household finance measures continued their second consecutive month of upward trajectory. Headlines from June showed that inflation was at 1.2% in June, surpassing previous expectations.

Livestock Markets

Pork

Over the past 12 weeks, total pig meat purchase volumes fell by 3.4% year-on-year to 32,619 tonnes, while spend declined by 2.7%, despite easing inflation. This reflects relatively stable pricing. Primary pig meat performed strongly, with volumes up 5.1% and spend increasing by 4.8% year-on-year. Growth was driven by key cuts, particularly mince, up 25.6% and roasting joints, up 12.6%, supported by increases in both shopper numbers and volumes per trip. This suggests pig meat continues to benefit from its position as a more affordable protein, with shoppers likely turning to pork options, especially mince, as a lower-cost alternative. By contrast, processed pig meat volumes declined by 5.8%, with losses on lines including bacon rashers, sausages and sliced cooked meats, mainly due to fewer shoppers and reduced purchase frequency.

Dairy

Milk volumes declined by 0.9% year-on-year, while average prices rose by 5.6%, resulting in a 4.6% increase in spend. Volume declines were recorded across semi-skimmed, skimmed and plant-based milk. Whole milk continued to grow, with volumes up 1.7% year-on-year. Other cow milk also saw strong growth, with volumes increasing by 15.9%, mainly driven by higher volumes purchased per shop.

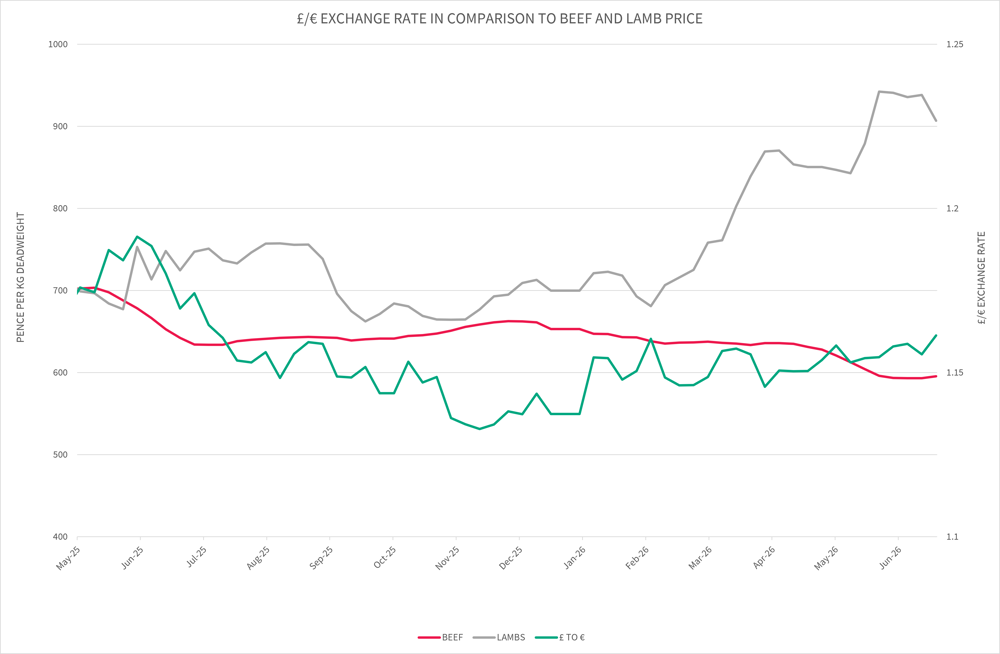

BEEF AND LAMB PRICE

Beef

Quarter 2 has shown the beef prices to be continuingly decreasing after their highs over the previous 12 months. Prices have finished the quarter at 595.60p/kg/dw for all steers, a 38p/kg/dw decrease compared to the end of last quarter.

Lamb

Lamb prices have seen an increase over quarter two despite their usual seasonal decline. The average lamb price (R3L) for June 2026 is 733.5p/kg/dw, a 197p/kg/dw increase compared to June 2025. Prices peaked at 942.5p/kg/dw in the week commencing 29 May and ended the quarter at 907p/kg/dw.

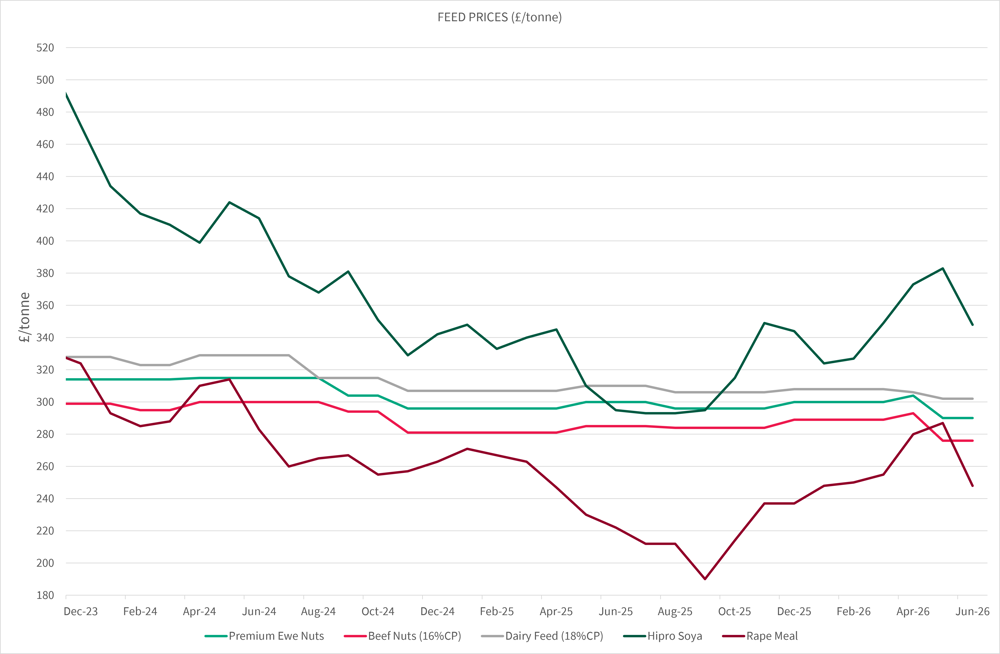

Feed

Dairy feed, premium ewe nuts and beef nuts have all decreased in price throughout the quarter.

Hipro soya and rape meal prices both spiked over the quarter; however, the prices returned to their normal levels, closing at £348/tonne for hipro soya and £248/tonne for rape meal (peaks of £383/t and £287/t respectively in May). Specifically, larger soybean harvests in South America and a potential US-China trade deal have contributed these price fluctuations throughout the quarter.

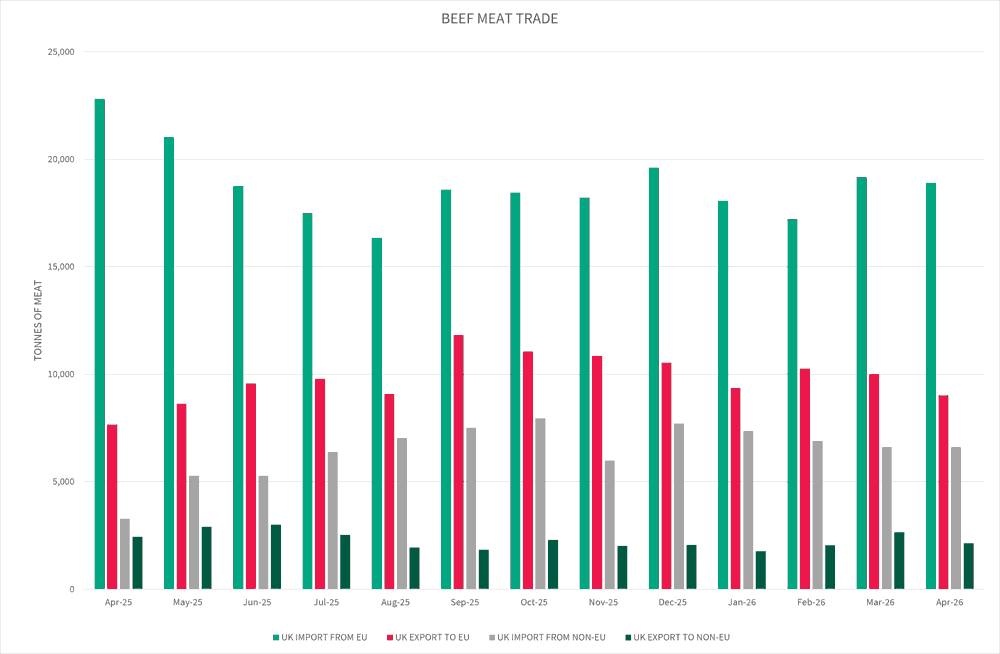

MEAT TRADE

The UK imports from non-EU increased by 101% in the past year from 3,280 tonnes in April 2025 to 6,603 tonnes in April 2026. Comparably, UK imports from EU has decreased by 12% from 22,801 tonnes in April 2025 to 18,896 tonnes in April 2026. The UK remains a net importer despite UK exports to EU increasing by 18% from April 2025 to April 2026.

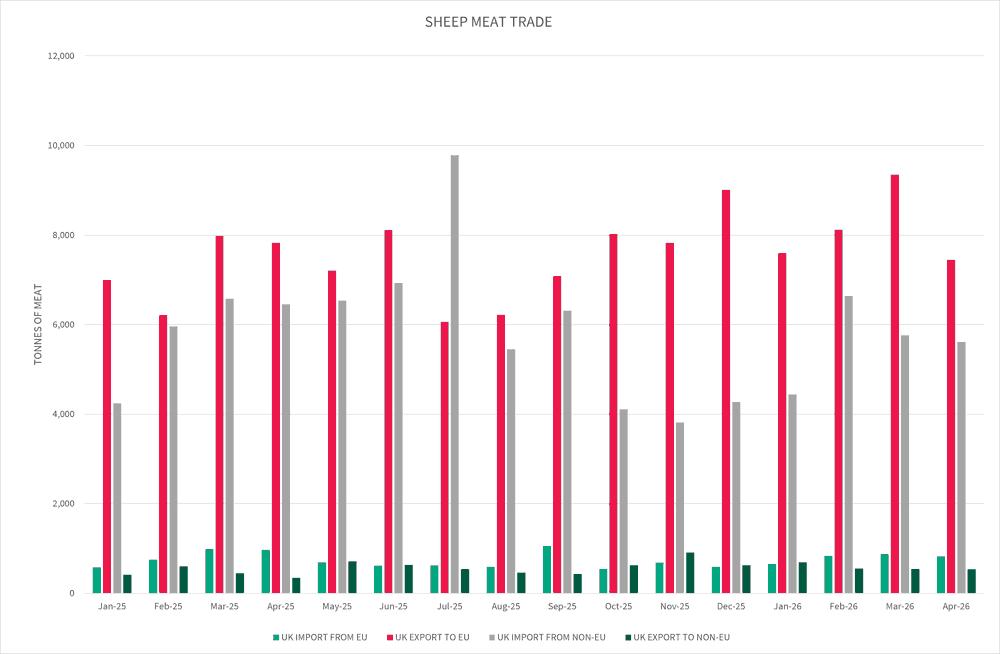

The most significant shift for sheep meat, is the 57% increase in UK export to non-EU countries from April 2025 (341 tonnes) to April 2026 (536 tonnes), with a 5% decrease seen in UK export to the EU. UK imports as a whole have decreased from April 2025 figures by 14%. The UK remained a net exporter in quarter two.

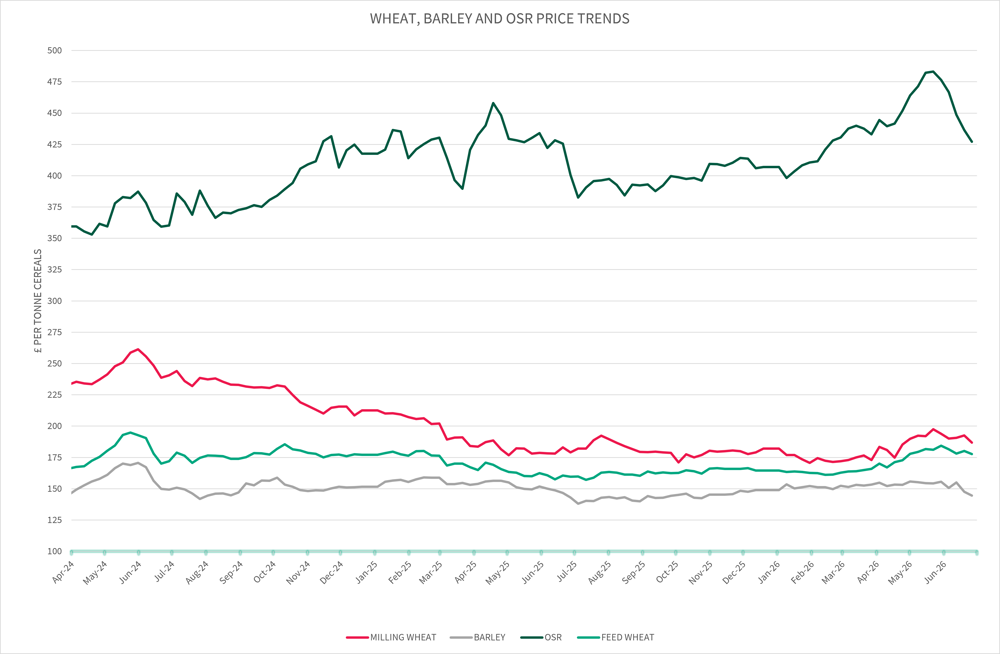

WHEAT, BARLEY AND OSR PRICE TRENDS

Feed wheat price has been gradually increasing, ending the quarter at £177.70/tonne, compared to £165.90/tonne at the end of the previous quarter.

Milling wheat price has followed the feed wheat trend by increasing, ending the quarter at £186.8/tonne. The milling premium has fluctuated over the quarter, ending at £9.10/tonne.

Oilseed rape price increased at the first half of the quarter, but then continually decreased during the second half, closing at £427.1/tonne, a decrease of £5.90/tonne from the end of the last quarter.

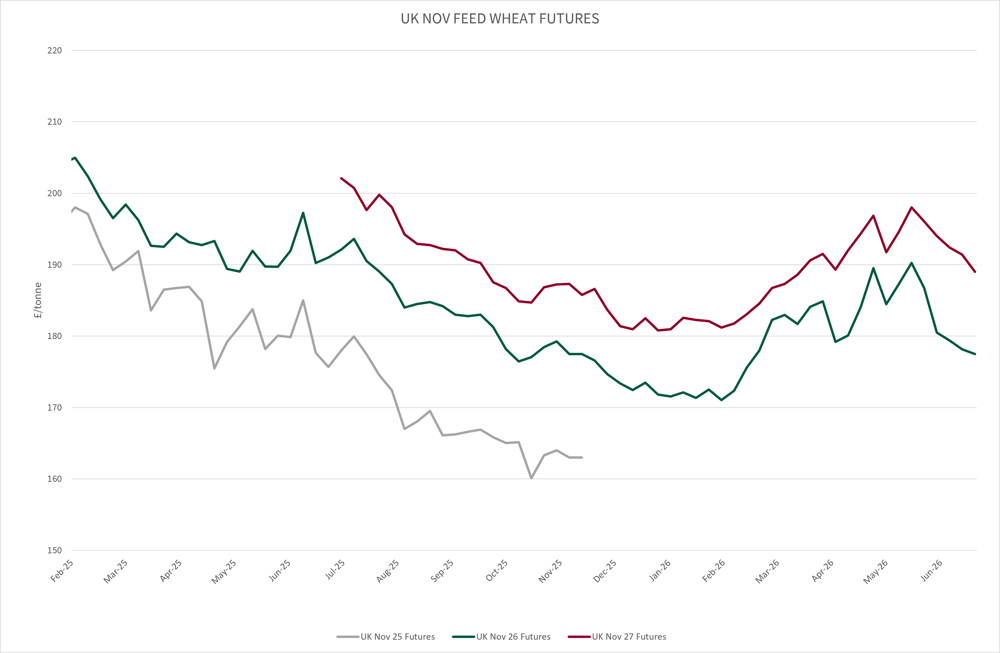

Futures Market

Both November 2026 and November 2027 wheat futures have peaked and fallen at a similar rate, closing the quarter for November 2026 at £177.50/tonne, a decrease of £6.60/tonne and November 2027 at £189/tonne, a decrease of £1.60/tonne.

INPUTS

Both Crude Oil and Red Diesel prices continued to increase at the start of quarter two, however, latterly the prices have begun to decrease.

Red Diesel ended the previous quarter at 117.08pence/litre, the price peaked early into quarter two in mid-April at 123.66pence/litre, however, the price continued to come down ending the quarter at 78.58pence/litre, a decrease of 38.5pence/litre.

Crude Oil saw a peak price of $103.43/barrel at the start of May 2026, however, has ended the quarter at $72.01/barrel, $15.06/barrel less than at the start of the quarter despite the highest prices mid quarter.

FERTILISER

Fertiliser prices on the whole have fluctuated over quarter.

34.5%AN started the quarter at £495/tonne and ended the quarter at £500/tonne, £5/tonne increase but has highs of £545/tonne in May. 0-24-24 has seen a £70/tonne increase since the end of the last quarter, ending at £485/tonne.

TSP has had the most dramatic increase starting the quarter at £505/tonne and ending at £650/tonne, up 28% due to the turbulence and unrest in the Middle East and the fertiliser needing to pass through the Strait of Hormuz.

Keep updated

Keep up-to-date with our latest news and updates. Sign up below and we'll add you to our mailing list.